What You Need to Know About the Student Loan Debt Relief Plan

Today I want to talk about the student loan debt relief plan. On August 24, we heard some major news about student loans. All of the official information is available at studentaid.gov, but I have gone through it and laid it out for your convenience.

Why should I care?

I think it is crucial for all of us to educate ourselves and make sure we understand what is happening. You should definitely stay informed if you have student loans, but even if not, it may be useful to prepare for what this may mean for the economy.

For a lot of us, this news may mean either that all of our student loan debt gets wiped out, or that the bulk of it does, and we can cover the rest with the money we have saved up. Many people have over six figures of student loan debt, and obviously in that case this change will not solve all your problems, but taking off $10,000 to $20,000 is still really significant.

What is the student loan debt relief plan?

The federal student loan debt relief plan consists of three parts.

Part 1: Final extension of the student loan repayment pause

The payment pause for student loan forbearance at 0% interest, which we have had for over two years now, is being extended for a final time through December 2022, so we can expect payments to resume in January 2023. It has been announced that this is the final extension.

We have heard that before, but there is reason to believe that this is truly the last extension, since this time there is cancellation mixed in here. Just like before, the pause is automatic: no application is required, you just will not need to make payments, and no interest will be occurring on your student loan debt.

Part 2: Targeted debt relief to low- and middle-income families

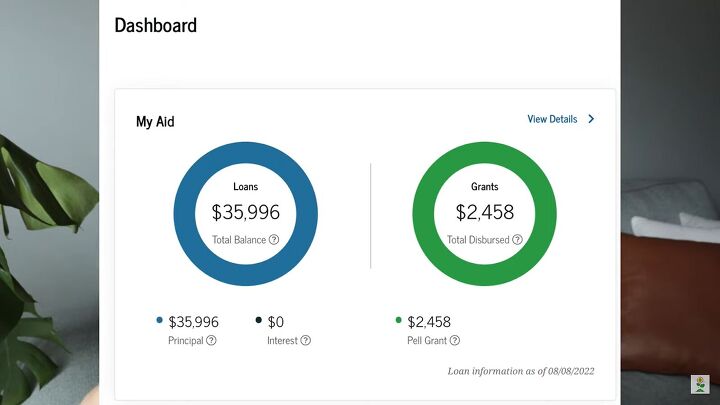

With this plan, you can get up to $20,000 of your debt canceled. Importantly, this is not a debt relief plan for any student loans, it is only relevant for federal loans, no matter if they come from undergraduate or graduate school.

Another condition is that your income is below $125,000, or under $250,000 if you are married. You can provide your income for either 2020 or 2021 when applying.

Finally, there is another requirement in place to be eligible for $20,000 cancellation as opposed to $10,000: you have to have received at least one Pell Grant while in college.

If you are not sure if you received one, go to studentaid.gov, log in and check your financial history, and you will see the Pell Grant right there. Provided you have received one and you meet the income limit, you are eligible for $20,000 of federal debt cancelation.

Another thing to pay attention to is the term “up to”: they say you can receive up to $10,000 or $20,000 of student loan debt cancellation. This means that if your debt is smaller than the amount of cancellation that you are eligible for, only the debt that you have left will be wiped out, there is no credit to be received on your account.

For example, if you qualify for $10,000 of cancellation but only have $8,000 of student loan debt left, then $8,000 will be wiped out.

If you have over $20,000 or $10,000, whichever you qualify for, you will get the respective amount canceled, and will have to pay the rest.

If you have paid student loans throughout the forbearance, you can request a refund on those. If you have recently paid off some of the debt, make sure to call your loan provider and take advantage of the forgiveness.

The website claims that about 8 million people will automatically get this cancellation. That can only happen if the Department of Education has your income data. If this is not the case for you, there is a simple application process. You can sign up at Subscriptions in order to get an email once the applications are available. You will have to submit the application before the end of the year.

Is there an income tax on this cancellation?

No. There was a covid relief plan, according to which there is no income tax on anything that is forgiven from the beginning of the pandemic until 2025. You might need to report having received a cancellation while doing your taxes though.

Part 3. Making the student loan system more manageable

There is a lot to discuss with this one, but I will be brief for now. With the reformed system, there is a capped percentage of payments for individuals with lower incomes. That way, for instance, you would not pay $500 a month when that makes up 5% of your income.

Public Service Loan Forgiveness plan

There have been some changes with the Public Service Loan Forgiveness plan, so if you are a public service worker, definitely look into it.

According to the new rules, even if you have been in your public service job for years and have not applied and made qualifying payments, you can still start now. The deadline to enroll is October 31, and this is an opportunity to get all of your debt wiped out.

This is especially relevant to those with larger amounts of student loan debt, and those planning to work in public service long term. You can find more information at PSLF.

When is the cancellation happening?

We do not know yet. No definite dates have been announced, so it may take a couple of weeks or multiple months. We will just have to stay updated with the student loan updates.

Since many of us do not have our income data registered with the Education Department, we will have to apply and wait for the applications to be processed. Let’s just keep an eye on our accounts.

Student loan debt relief plan

As I said, this student loan debt relief plan is a game-changer for a lot of people, making many debt-free. I hope that this article helped you understand the changes better and take advantage of them.

This relief potentially just freed up 10, 15, or even 20 years of payments for us, and we will now have money to put toward other goals. What are your priorities once you are debt-free? Let us know in the comments.

Comments

Join the conversation

What if I had my student loans consolidated? Would I still qualify?

With a six figure bill it sure would be nice to knock off 20k bút ít looks like they are ignoring anyone who is out of the country. When I click on the link I get a message telling me the link is not available. 🥲