Do I Need More Than $1,000,000 for Retirement?

Have you ever had the goal of having $1,000,000 for retirement? If you have, you're not alone, as it is a common goal in the financial community. People often say a million dollars isn't what it used to be. The fact of the matter is it's true. The main reason is inflation, something we're all a little too familiar with.

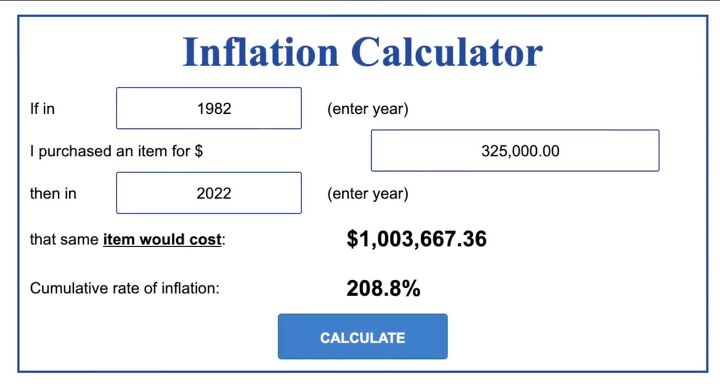

1982

What if we were to rewind 40 years to 1982?

Let's say you've saved a million dollars, retire on that, and you apply the rule of 4%, and live off $40,000 a year. That's a pretty impressive nest egg that would provide a pretty comfortable lifestyle.

2022

Then let's come back to the present day. It's 2022. How much would you need to have that same standard of living as someone who retired in 1982 with that million dollars? You would need a nest egg of roughly $3.1 million.

Put another way, $1 million in 2022 is roughly equivalent to a $325,000 nest egg in 1982.

That $40,000 income in 1982 would be like living on $124,000 a year today. So basically, the value of money was cut to a third over those four years. Knowing that can be helpful to know when you're planning your future using that line of thinking.

How much should I save for retirement?

A recent analysis from Seeking Alpha said that millennials are going to need anywhere from 3 to 4 million to retire comfortably, saying that those more senior millennials around the age of 40 would need about 2.8 million to step away from the workforce and those younger millennials would probably need closer to 3.6 million.

Inflation & Social Security

While the primary reason for these lofty numbers is inflation, the other contributing factor is the uncertainty that surrounds Social Security as it stands today. Without any changes, the Social Security Trust is set to become insolvent by the year 2035.

Changes will be made to the present system; I don't think the whole system will go belly up. It's probably safe to assume the younger you are, the less you should count on Social Security being a significant source of income for you in retirement.

Let's go back to the numbers, that $3,000,000 or $4,000,000. Those are pretty hefty amounts. I don't think they're unreasonable, but I do think they're pretty hefty amounts to recommend to entire generations.

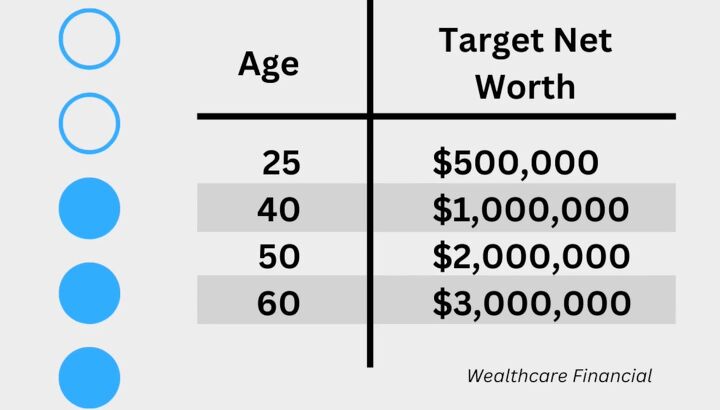

Wealthcare Financial gave benchmark recommendations for net worth at various ages for Gen Z and Millennial members to stay on track to hit this $3,000,000 goal.

They'll need $500,000 by the age of 25, $1,000,000 by the age of 40, $2,000,000 by the age of 50, and $3,000,000 by the age of 60.

There is something amiss with these targets because that's not how compounding works. It is very slow to get it moving in the beginning, but over time it starts to accelerate and snowball.

So when I see that the first target is to hit half a million dollars at 25, most people probably graduate around 21. So that means you probably have four working years, probably your lowest earning years, to stash away half a million dollars.

I don't know how realistic that is. You can house hack all you want; you can side hustle. I don't think for most people, that's possible. They give you 15 years to double your money and hit a million. It seems like those numbers are off.

Benchmarks

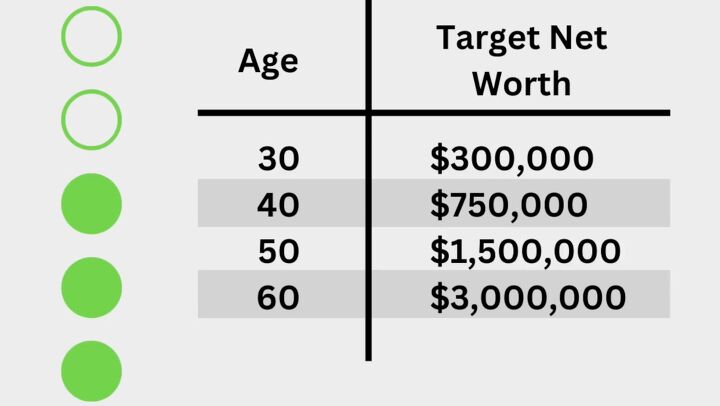

If I was going to have the goal of hitting $3,000,000 by retirement age, here are the benchmarks I might use.

$300,000 by the age of 30. $750,000 by the age of 40, 1.5 million by the age of 50, and $3,000,000 by the age of 60.

It is just the hardest to save that first million. Each subsequent million milestone gets incrementally easier because you have money invested and working for you.

You are doing the vast majority of the legwork for those initial amounts saving that first $100,000 or that first $500,000. It is the amount of money that you are stashing away in your savings and investments that matters.

As time goes on and you have more put away into investments, that's when you start to notice compound interest doing its magic and doing the brunt of the leg work.

There is no doubt that inflation has a significant impact on what your money can buy. When it comes down to it, saying that if you're going to retire in 30 years, you're going to need 3 or 4 million stems from the same mentality where people say you need to have a million dollars to retire today.

The people who believe this took that million-dollar number, extrapolated it, and factored in inflation.

Lifestyle

How much you need to retire is very individual and based on your lifestyle; if you enter retirement completely debt free, including no mortgage, you may be looking at a very low-cost retirement.

Also, the activities you want to do and how much you want to travel will also play a huge factor.

These blanket rules don't consider alternative retirements like people who downsize their home and go to a more affordable location or people who engage in geo arbitrage and pick up their life and move to an entirely different country to capitalize on a lower cost of living.

To say that every retiree today needs a million dollars to retire is inaccurate and misses the point of individual needs. Thirty years from now, some will need more; some will need less.

Will they need three or $4,000,000? Some will. Some will need more; some will need less.

Do I need more than $1,000,000 for retirement?

For super savers, achieving a net worth of $1 million probably seemed like a very audacious goal in 1982. Just like achieving a net worth of three or $4 million seems like an audacious goal today.

But if you give yourself enough of a runway, if you put your head down, you'll work hard, you grow your income, you save, you invest, you can probably get there.

Are you working towards having $1,000,000 for retirement? How are you making that happen? Share your experience in the comments below.

Comments

Join the conversation